Have you ever wondered if your car insurance still applies when you move to a new state or drive across state lines? Many drivers assume their current policy will follow them, but that’s not always the case. States have different insurance requirements, and failing to update your coverage can leave you unprotected and facing legal issues.

Imagine getting into an accident in a new state, only to discover your insurance isn’t valid because you didn’t update your policy. Not only could you be financially responsible for the damages, but you could also face legal consequences for not complying with state laws. Whether you’re moving, road-tripping, or studying away from home, the risks are real.

The good news is that understanding state-specific car insurance rules is simpler than it seems. In this guide, we’ll break down the laws in each state, what you need to do to stay covered, and how to avoid costly mistakes. From road trips to relocating, we’ve got you covered with all the info you need to ensure your car insurance is valid wherever you go.

The Golden Rule: Car Insurance Is State-Specific

So, is car insurance state-specific? The answer is an unequivocal yes. The United States does not have a single, federal law that governs auto insurance. Instead, each of the 50 states and Washington D.C. sets its own laws and regulations. This is why you cannot simply buy a policy from another state because it’s cheaper—doing so is a form of insurance fraud.

Your car insurance policy is directly tied to the state where your vehicle is registered. This state is considered your primary residence, the place where your car is garaged most of the time. Insurance companies use your location as a primary factor in calculating your premium because the risks associated with driving, such as traffic density, weather patterns, and rates of theft and vandalism, vary significantly from one state to another, and even from one ZIP code to another.

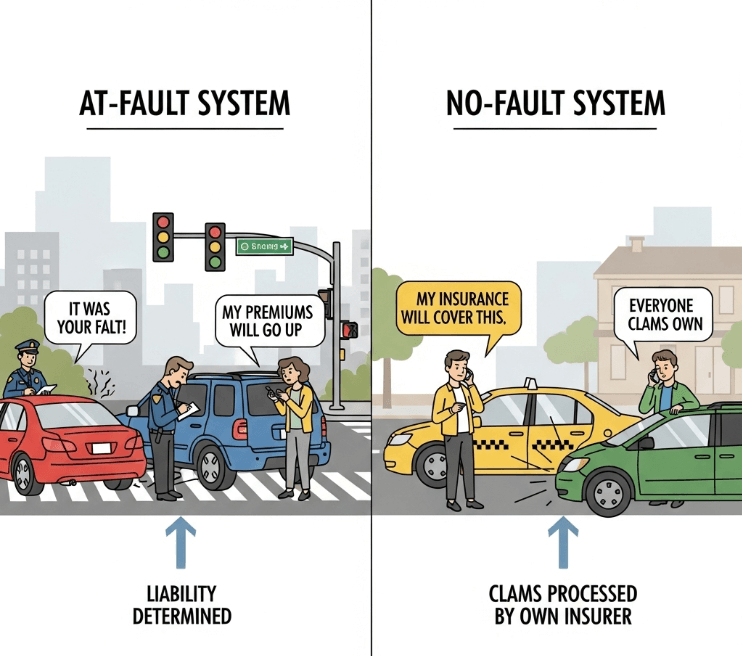

The Legal Foundation: At-Fault vs. No-Fault States

One of the most significant differences between states is the legal framework they use to handle accidents and injuries. This system determines whose insurance company pays for damages and medical expenses after a crash. Every state follows one of two systems: at-fault or no-fault.

At-Fault States

The majority of states are at-fault states. In this system, the driver who is legally determined to have caused the accident is responsible for paying for the other party’s damages and medical bills. This is why liability insurance is a cornerstone of car insurance requirements in these states. If you cause an accident, your liability coverage pays for the other person’s expenses up to your policy limits. If the costs exceed your limits, you could be held personally responsible for the remaining amount.

No-Fault States

In a no-fault state, your own car insurance policy will cover your medical expenses and lost wages, up to a certain limit, regardless of who caused the accident. This is accomplished through a coverage called Personal Injury Protection (PIP). This system was designed to reduce the number of lawsuits related to minor injuries and to ensure that individuals receive prompt medical care without having to wait for a lengthy fault determination process.

Currently, the following are no-fault states:

- Florida

- Hawaii

- Kansas

- Kentucky

- Massachusetts

- Michigan

- Minnesota

- New Jersey

- New York

- North Dakota

- Pennsylvania

- Utah

It is important to note that even in no-fault states, the at-fault driver is still typically responsible for property damage. Furthermore, if injuries are severe and exceed the state’s threshold, the injured party may still be able to sue the at-fault driver for additional damages.

Building Your Policy: Common Types of Required Coverage

Because insurance is state-specific, the types and amounts of coverage you are required to carry can vary significantly. While some coverages are nearly universal, others are only required in certain states.

| Coverage Type | What It Covers | Who Requires It |

| Bodily Injury Liability | Injuries to other people (drivers, passengers, pedestrians) that you cause in an accident. | Required in almost every state (except New Hampshire). |

| Property Damage Liability | Damage to another person’s property (their car, fence, etc.) that you cause in an accident. | Required in almost every state (except New Hampshire). |

| Personal Injury Protection (PIP) | Your own and your passengers’ medical expenses and lost wages, regardless of who is at fault. | Required in all no-fault states. |

| Uninsured/Underinsured Motorist (UM/UIM) | Your medical expenses and, in some states, vehicle repairs if you are hit by a driver with no insurance or not enough insurance. | Required by about half of the states. |

| Medical Payments Coverage (MedPay) | Your and your passengers’ medical expenses resulting from an accident, regardless of fault. | Only required in Maine, but offered as an optional coverage in many other states. |

Beyond these, coverages like Collision (which covers damage to your own car from a crash) and Comprehensive (which covers non-crash-related damage like theft, fire, or storm damage) are typically optional, but may be required by a lender if you have a loan or lease on your vehicle.

Crossing State Lines: How Your Insurance Protects You on the Road

If your car insurance is tied to your home state, what happens when you take a road trip? Fortunately, you are still covered. This is thanks to a provision in most auto insurance policies known as the “broadening clause.”

This clause automatically adjusts your coverage to meet the minimum liability requirements of any other state you are temporarily driving in. For example, if your home state requires $15,000 in property damage liability, but you drive into a state that requires $25,000, your policy will automatically provide the higher $25,000 limit in the event of an accident in that state. This ensures you are always driving with legal levels of insurance, no matter where you are in the U.S.

Driving Internationally

- Canada: Most U.S. auto insurance policies extend coverage to you when you are driving in Canada. It’s always a good idea to bring your insurance ID card and to notify your insurer of your travel plans.

- Mexico: Your U.S. policy will not cover you in Mexico. To be legally protected, you must purchase a separate, short-term Mexican auto insurance policy from a licensed Mexican insurer. Many U.S. insurance companies have partnerships that make it easy to purchase this coverage before your trip.

Life in Motion: Insurance for Complex Living Situations

While the rules for temporary travel are straightforward, what happens when your living situation is more complex? Here’s how insurance works for common scenarios.

Permanently Moving to a New State

When you make a permanent move, you must update both your vehicle registration and your car insurance to your new state. Insurers require this because your new location has a different risk profile, which will affect your premium.

Most states provide a grace period, typically between 30 and 90 days, for you to complete this process. Here are the general steps:

- Contact your current insurer: Inform them of your move. If they operate in your new state, they can help you transition your policy. If not, you will need to find a new insurance carrier.

- Shop for new insurance: Get quotes from several companies in your new state to find the best coverage and rates.

- Purchase your new policy: Ensure your new policy is active before you cancel your old one to avoid any lapse in coverage.

- Update your registration: Take your proof of new insurance to your new state’s Department of Motor Vehicles (DMV) to register your vehicle.

- Cancel your old policy: Once your vehicle is registered and your new policy is active, you can safely cancel your previous policy.

College Students Studying Out-of-State

For college students, the primary question is one of residency.

- Without a Car: If a student is attending college out of state but does not take a car with them, they can typically remain on their parents’ policy. In fact, the family may be eligible for a “student away at school” discount if the college is more than 100 miles from home.

- With a Car: If a student takes a car to school in another state, the situation is more nuanced. If their primary residence is still considered their parents’ home (meaning they return during breaks), they can often remain on the family policy. However, it is crucial to notify the insurance company of the car’s new location, as this will likely affect the premium. If the student establishes permanent residency in the new state, they will need to obtain their own insurance policy and register the car there.

Military Members Stationed Elsewhere

Active-duty military members often have more flexibility. Due to the nature of their service, most states allow them to maintain their car insurance and registration in their home state of record, even when they are stationed in another state for an extended period. However, upon a Permanent Change of Station (PCS), it is always wise to consult with your insurance agent to confirm that you are meeting all legal requirements and have adequate coverage.

Dual Residency and “Snowbirds”

Individuals who split their time between two states, such as retirees who spend winters in a warmer climate, must establish one state as their primary residence. This is typically the state where you spend more than half the year (183 days or more). Your car should be registered and insured in this primary state.

If you own and keep vehicles at both residences, you will likely need two separate insurance policies—one for each state, reflecting where each car is primarily garaged.

The Pitfalls of Misrepresentation: Insurance Fraud

Given that insurance rates can vary dramatically from one state to another, it can be tempting to register and insure your car at a relative’s address in a cheaper state. However, this is a form of insurance fraud known as rate evasion.

Insurance companies have sophisticated methods for verifying addresses. If you are caught, the consequences can be severe:

- Denial of a claim: If you get into an accident, your insurer can deny your claim, leaving you responsible for all costs.

- Policy cancellation: Your provider will cancel your policy, which can make it harder and more expensive to get insurance in the future.

- Legal penalties: You could face fines and, in some cases, even criminal charges.

The rule is simple: be honest about your primary address. The short-term savings are not worth the long-term financial and legal risks.

Frequently Asked Questions (FAQs)

Q: How soon do I need to get a new car insurance policy after I move?

A: Most states require you to update your insurance and registration within 30 to 90 days of establishing residency. It’s best to contact your new state’s DMV for the exact timeframe. Always secure a new policy before canceling your old one.

Q: Can I have two car insurance policies in different states?

A: Generally, you cannot have two policies for the same car. However, if you own two different cars that are primarily kept in two different states (e.g., a primary home and a vacation home), you will need two separate policies, one for each vehicle in its respective state.

Q: What happens if I get a traffic ticket in another state?

A: Thanks to interstate agreements like the Driver License Compact (DLC), your home state will almost certainly be notified of the violation. You will be responsible for resolving the ticket with the state where it was issued to avoid penalties like license suspension in your home state. A ticket in another state can also lead to an increase in your insurance premium upon renewal.

Q: Is Car Insurance State-Specific?

A: Yes, car insurance is state-specific. Each state in the U.S. has its own insurance requirements and regulations, meaning your current policy may not meet the legal standards in a new state. When moving or traveling across state lines, you must update your car insurance to comply with local laws and coverage needs. Failure to do so can lead to fines, policy cancellations, or denied claims. Make sure to review state-specific rules, minimum coverage requirements, and consider shopping for new insurance quotes when relocating.

Q: Why are my insurance rates changing so much just from moving to a new state?

A: Insurance rates are based on risk. Factors like population density, traffic congestion, crime rates, weather events, and the number of claims in a given area all contribute to this risk profile. Moving from a rural area to a major city, or from a state with low minimum coverage requirements to one with higher requirements, will almost always result in a change in your premium.

By understanding the state-specific nature of car insurance and following the proper procedures for your unique situation, you can ensure that you are always legally protected, no matter where your journey takes you.