Are you juggling insurance for a daily driver, a weekend classic, or perhaps a new car for your college-bound student? You may find yourself asking a surprisingly common question: “Can I have multiple car insurance policies?”

The thought of managing more than one policy can seem complicated. You might wonder if it’s legal, if it provides better coverage, or if it will simply drain your wallet. Many people find themselves in situations where a single policy doesn’t seem to fit—perhaps you own a business vehicle, or you want to help your girlfriend insure her first car without adding a high-risk driver to your pristine record. The simple truth is that while having multiple policies is possible, doing it wrong can lead to serious legal and financial trouble.

Imagine having complete clarity on your car insurance. Imagine knowing exactly how to structure your policies to get the best possible coverage at the lowest price, without the fear of making a costly mistake. This guide will give you that confidence. We will break down the rules in simple, easy-to-understand language, showing you when multiple policies are a smart financial move and when they are a trap. You will learn the key terms that empower you to speak confidently with insurers and make the best decisions for your unique situation.

Read on to learn everything you need to know about navigating the world of multiple car insurance policies, ensuring you and your vehicles are protected correctly and affordably.

The Core Question: Can You Have Multiple Car Insurance Policies?

Let’s get straight to the point: Yes, you can legally have multiple car insurance policies.

However, there is a crucial distinction that you must understand. This “yes” comes with a fundamental rule: you can have different insurance policies for other cars, but you generally cannot have multiple insurance policies for the exact vehicle.

This single rule is the foundation of how multiple car insurance policies work. Trying to ensure the exact vehicle twice is not only impractical but can also lead to accusations of insurance fraud. On the other hand, strategically using different policies for different vehicles can sometimes be the most innovative and most cost-effective solution.

This guide will walk you through both sides of this rule, helping you understand when to seek multiple policies and when to consolidate them.

The Golden Rule: One Car, One Primary Policy

It might seem like having two insurance policies on your Honda Civic would mean you get double the payout if it’s totalled. Unfortunately, it doesn’t work that way. Insuring a single vehicle with two separate standard auto insurance policies is something that insurance companies actively prevent, and for good reason.

Understanding “Unjust Enrichment” and Insurance Fraud

The core principle at play here is called unjust enrichment. In simple terms, insurance is designed to make you “whole” again after a loss, not to help you profit from it.

- Example of Unjust Enrichment: Imagine your car sustains $4,000 in damage from a hailstorm. If you had two comprehensive insurance policies, you could not file a claim with both and receive a total of $8,000. Doing so would mean you profited $4,000 from the incident, which is illegal.

Filing two claims for the same damage on a single vehicle is considered insurance fraud. This is a serious offence that can lead to:

- Cancellation of both policies.

- Denial of your claim.

- Difficulty obtaining insurance in the future.

- Potential felony charges and legal penalties.

How Do Insurance Companies Know?

You might wonder how two different companies would find out. Insurance providers share information through industry databases. When you register your car with the Department of Motor Vehicles (DMV), you must provide proof of insurance. Suppose two different policies are linked to the same Vehicle Identification Number (VIN). In that case, it will raise a red flag in these shared systems, and one or both insurers will likely cancel your coverage.

Key Takeaway: The fundamental purpose of insurance is to cover a loss, not create a profit. Therefore, you can only have one primary liability policy per vehicle.

When It Makes Sense to Have Different Car Insurance for Different Cars

While insuring one car twice is a bad idea, there are many legitimate and even necessary situations where you would have multiple auto policies. This is where our LSI keyword, “can you have different car insurance for different cars,” becomes highly relevant.

Here are the most common scenarios where multiple policies are the right choice:

1. Insuring a Classic, Collector, or Luxury Car

If you own a pristine 1967 Ford Mustang or a high-end luxury vehicle like a Porsche 911, a standard auto policy might not be enough. These cars have unique needs that are best met by a separate, specialised policy.

- Agreed Value vs. Actual Cash Value: Standard policies pay out the “actual cash value” of a car, which includes depreciation. For a classic car, this would be a fraction of its true worth. A speciality classic car policy provides agreed value coverage, where you and the insurer agree on the car’s value upfront.

- Specialised Insurers: Companies like Hagerty, Grundy, and American Collectors Insurance specialise in these vehicles and understand their unique risks and repair costs. It is often cheaper and more effective to have a speciality policy for your collector car and a separate, standard policy with a company like GEICO or Progressive for your daily driver.

2. Separating Business and Personal Vehicles

If you use a vehicle primarily for work, your auto policy may not cover it.

- Personal vs. Commercial Use: An individual policy is for commuting, errands, and leisure. A commercial policy is for vehicles used for transporting goods, visiting clients, or other business-related activities.

- Example: A plumber who uses a Ford Transit van for work should have that van on a commercial auto policy. Their family’s Toyota RAV4 should be on a separate personal auto policy. If the truck is involved in an accident while on a job, the individual policy would likely deny the claim.

3. Insuring High-Risk Vehicles Separately

If you own a high-performance sports car, its insurance premium can be extremely high. If you add it to a policy with your other “tamer” vehicles, it could significantly increase the overall cost. In some cases, it may be more economical to get a separate policy for the high-risk car, mainly if it’s not driven often, to isolate its high premium from your other vehicles.

4. Drivers or Vehicles in Different Households or States

Insurance policies are based on risk, and a primary factor is where the vehicle is “garaged” or parked overnight.

- College Students: If your child attends college in another state and has a car with them, they will likely need a separate insurance policy in that state that reflects the local address and state-specific coverage requirements.

- Multiple Residences: If you own a vacation home in another state and keep a car there, that vehicle will need its policy registered to that address.

5. High-Risk Drivers in the Household

This is a more complex but sometimes necessary reason for separate policies. If you have a driver in your household with a poor driving record (multiple accidents, DUIs) or a very low credit score, adding them to your policy can cause your premiums to skyrocket.

In some states, you can create a separate policy for that individual and their vehicle and have them listed as an excluded driver on your policy. This is a complicated process and not allowed in all states, so it’s crucial to speak with an insurance agent to see if it’s a viable option.

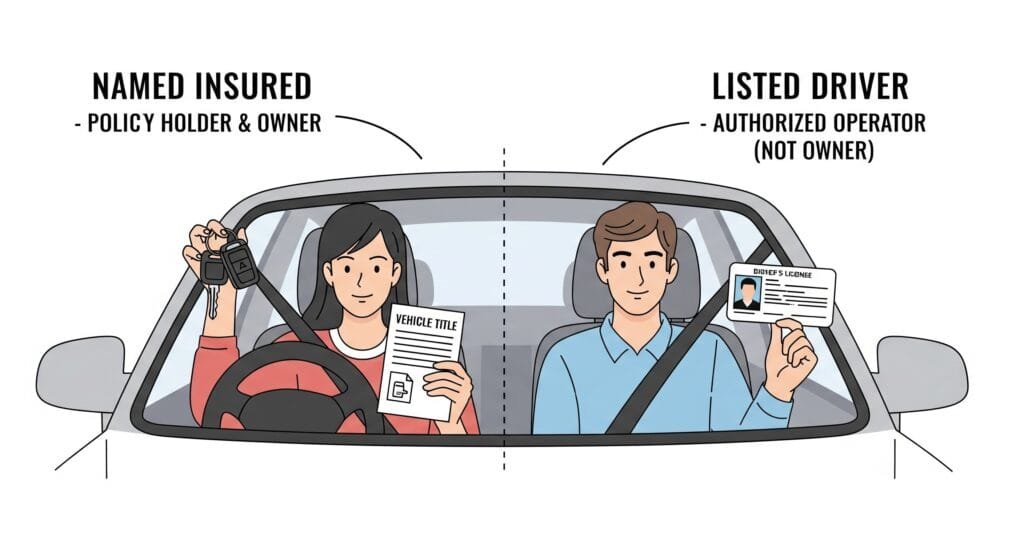

The Most Important Terms to Understand: Listed Driver vs. Named Insured

Much of the confusion around multiple policies stems from not understanding the difference between being a “named insured” and a “listed driver.” Getting this right is the key to being covered adequately across different policies.

What is a Named Insured?

The named insured is the person or people who own the insurance policy. Think of them as the primary contract holder.

- They are responsible for paying the premiums.

- They are the ones who can make changes to the policy.

- In almost all cases, the named insured must also be the legal owner of the vehicle listed on the policy. This is known as having an insurable interest.

You can’t buy a policy for your neighbour’s car because you don’t have a financial stake in it. Your name is on the title, so your name must be on the policy as the named insured.

What is a Listed Driver?

A listed driver (sometimes called a “rated driver”) is anyone who lives in your household or regularly drives your vehicle but is not the policy owner.

- They are covered by the policy when driving the insured vehicle.

- They do not own the policy and cannot make changes to it.

- Their driving record, age, and other factors will be used to calculate the policy’s premium.

This is the most common and correct way to be on multiple policies.

- Real-World Example: Let’s use the scenario from the Reddit thread. The original poster drives a car that his parents legally own.

- On his parents’ policy, his parents are the named insureds, and he is a listed driver.

- He also wants to drive his girlfriend’s car. Her car is in her name.

- On her girlfriend’s policy, she is the named insured. If he drives her car regularly, he should be added as a listed driver.

In this scenario, he is legally and correctly covered by two different insurance policies for two other cars without committing any fraud.

The Smart Alternative: The Power of a Single, Bundled Policy

While there are valid reasons for multiple policies, for most households, the most financially savvy approach is to have a single policy that covers all vehicles and drivers. This is because insurance companies offer significant discounts for consolidation.

Multi-Car Discounts

Insuring more than one vehicle with the same company almost always results in a multi-car discount. Insurers reward this loyalty because it simplifies their risk management and administrative work. This discount can be substantial, often saving you up to 25% on your total premium.

Multi-Policy (Bundling) Discounts

The savings can be even greater if you “bundle” your car insurance with other types of policies from the same company. Common bundles include:

- Auto + Homeowners Insurance

- Auto + Renters Insurance

- Auto + Life Insurance

Bundling can offer some of the steepest discounts available in the insurance industry.

Understanding Permissive Use

What if you just want to let a friend borrow your car for a weekend? Do you need to add them to your policy? In most cases, no. This is covered by the permissive use clause found in most standard auto policies.

- What It Is: Permissive use extends your insurance coverage to someone who does not live with you but is driving your car with your permission on an infrequent basis.

- When It Applies: It’s for occasional use, such as letting a neighbour borrow your truck to move a piece of furniture.

- When It Doesn’t Apply: If someone starts driving your car regularly (e.g., a few times a week to commute), they are no longer an “occasional” driver. At that point, they must be added to your policy as a listed driver. Failing to do so can be considered misrepresentation and could lead to a claim being denied.

Potential Pitfalls and How to Avoid Them

Managing multiple policies, even when done for legitimate reasons, can have some downsides.

- Accidental Double Coverage: This can happen if you switch insurance companies and forget to cancel your old policy. The old policy might auto-renew, leaving you paying two premiums for the same car. Always confirm in writing that your old policy has been cancelled.

- Complicated Claims: If you are a listed driver on two different policies and get into an accident, determining which policy is primary and which is secondary can sometimes cause delays. Typically, the insurance follows the car, but coordination between companies may be required.

- One Accident, Multiple Premium Hikes: If you are a listed driver on your parents’ policy and your girlfriend’s policy, and you cause an accident while driving her car, both insurance companies may raise their rates at renewal because your driving record now shows an at-fault accident.

Final Checklist: Do You Need Multiple Policies?

Ask yourself these questions to decide on the best path forward:

- Who owns the car? The legal owner must be the named insured.

- Who drives the car regularly? Anyone who frequently drives a vehicle should be listed as a driver on that car’s policy.

- Are there unique circumstances? Do you have a classic car, a business vehicle, or a high-risk driver in the household?

- Have you compared quotes? Get quotes for both a single, bundled policy and separate policies to see which offers a better combination of price and coverage.

By understanding these key principles, you can confidently structure your car insurance to protect yourself and your vehicles without paying for unnecessary coverage or running into legal trouble.